Section 12.9 Prediction with ARIMA

The object returned by

ARIMA provides a method called get_forecast that generates predictions. To demonstrate, we’ll split the time series into a training and test set, and fit the same model to the training set.

training, test = split_series(nuclear)

model = tsa.ARIMA(training, order=order, seasonal_order=seasonal_order)

results_training = model.fit()

We can use the result to generate a forecast for the test set.

forecast = results_training.get_forecast(steps=len(test))

The result is an object that contains an attribute called

forecast_mean and a function that returns a confidence interval.

forecast_mean = forecast.predicted_mean

forecast_ci = forecast.conf_int()

forecast_ci.columns = ["lower", "upper"]

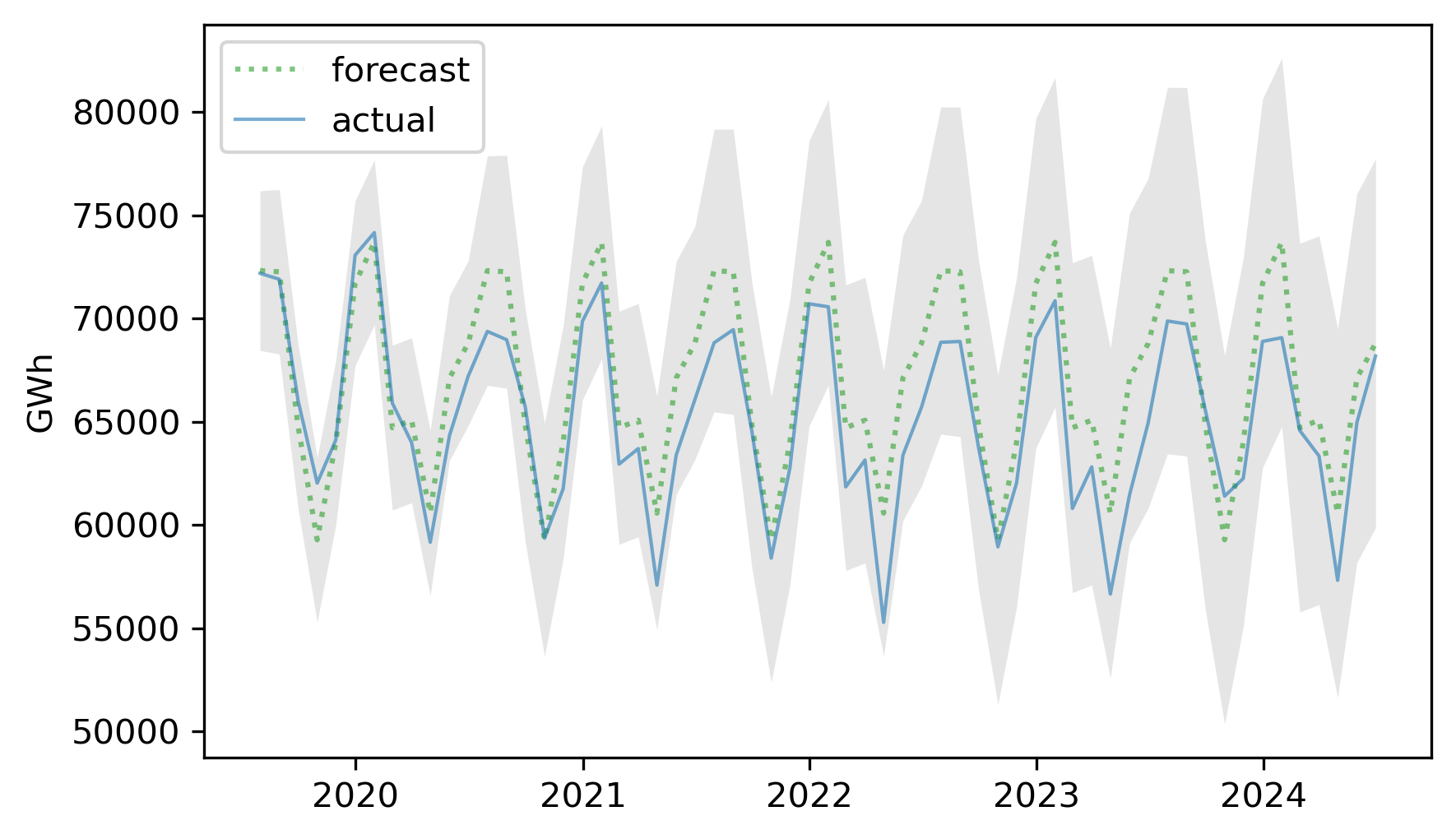

We can plot the results like this and compare them to the actual time series.

plt.fill_between(

forecast_ci.index,

forecast_ci.lower,

forecast_ci.upper,

lw=0,

color="gray",

alpha=0.2,

)

plt.plot(forecast_mean.index, forecast_mean, label="forecast", **pred_options)

plt.plot(test.index, test, label="actual", **actual_options)

decorate(ylabel="GWh")

The actual values fall almost entirely within the confidence interval of the predictions. Here’s the MAPE of the predictions.

$ MAPE(forecast_mean, test)

np.float64(3.3817549248044547)

The predictions are off by 3.38% on average, somewhat better than the results we got from seasonal decomposition (3.81%).

ARIMA is more versatile than seasonal decomposition, and can often make better predictions. In this time series, the autocorrelations are not especially strong, so the advantage of ARIMA is modest.